I wrote about 401(k) in another post (here), and I wanted to double down on one point…

I love 401(k)! Believe me when I say that it doesn’t even take a full 45-year career to become a 401(k) millionaire. You can really get there in half the time. Some of the key ingredients to success here are:

1) put away everything you can up to the max,

2) take advantage of any employer matching,

3) invest in low cost index funds (easiest is probably to do a target retirement fund that adjusts the mix of stocks and bonds as you get closer to retirement),

4) do it consistently year after year, and,

5) for crying out loud, DON’T TOUCH IT before retirement unless you absolutely have to!

In my other post, I wrote about the penalty you have to pay if you withdraw before the age of 59.5. I think the biggest penalty of an early withdrawal is not the fee you pay at the time (at least 10%). The biggest penalty is preventing yourself from getting wealthy. As Charlie Munger famously said, “The first rule of compounding: Never interrupt it unnecessarily.”

If this Charlie Munger quote is the only financial lesson I teach my kids, but they really understand and internalize it, they’ll be alright. It really is that important and could mean the difference between retiring as a millionaire or retiring with nothing but regret.

I want to illustrate the power of buying and holding. As Warren Buffett says, “our favorite holding period is forever.”

I also want to talk about buying household names that you know and understand. This idea that you can invest in companies whose products and services you use every day is something popularized by Peter Lynch, who is one of the most successful investors of our time (he managed the Fidelity Magellan Fund to an average annual return of 29.2%, making it the best-performing mutual fund in the world at the time). His philosophy was “invest in what you know,” and it’s actually very similar to the idea of investing within your “circle of competence,” which was popularized by Warren Buffett.

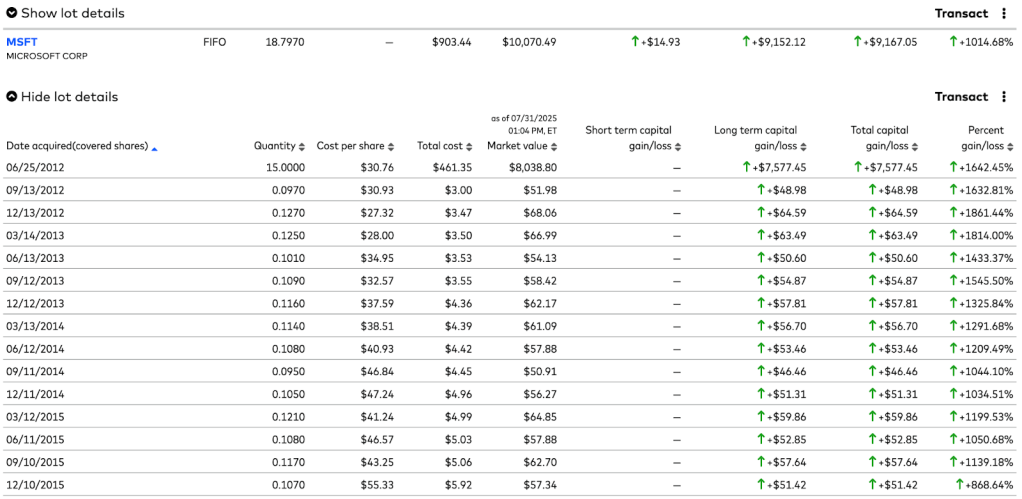

Onto my illustration… Microsoft and Meta (formerly Facebook) reported their quarterly results yesterday. Those results were very good for both companies, and so their stock prices jumped during the next trading day (Microsoft was up ~4% and Meta was up ~12% at some point during the day).

Well, roughly 13 years ago, as a regular happy user of the products of both companies, I happened to purchase some shares in both of these companies (15 shares of Microsoft and 25 shares in Meta). I also happened to hold these shares and not sell them. As the time went by, Microsoft’s share price increased and it paid out a quarterly dividend, which I automatically re-invested right back into the company. Same happened with Meta, though it only started paying a dividend in 2024.

When I bought Microsoft stock, the shares were priced at $30.76, so I paid a total of $461.35 for the 15 shares. Today, those same Microsoft shares are valued at ~$536 per share and $8K for the 15 shares (up 1,642%). If I include dividends, my Microsoft shares are valued at around $10K. Note that the dividends also grew at high rates.

Meta stock cost $20.28, so I paid $507 for the 25 shares. Today, Meta shares are valued at ~$778 per share and ~$19.5K for the 25 shares (up 3,737%). If I include dividends, my Meta shares are valued at around $19.6K.

Both companies are in the technology space, which is known for high growth. However, Microsoft is a 50 year old company (founded in 1975) and Meta is a 21 year old company (founded in 2004). Though I bought Meta in the year it went public, I bought Microsoft about 26 years after it went public. I wasn’t an early investor in either of these companies. Though I didn’t make retirement money there, I think it’s intellectually exciting to be able to generate a gain of 1,600%+ in a 50 year old company 26 years after its IPO.

This is how a few winners can make up for some duds.

Of course, the market has been very hot and some of these gains are driven by the overall stock market performance. That said, these companies have executed really well, managing existing core business and staying on top of innovation. A lot of people at these companies contributed to this success, but the leaders at the top play a critical role (CEO Satya Nadella at Microsoft and CEO Mark Zuckerberg at Meta).

Thank you, Satya and Mark. Best wishes for the next 12 years.

The point? Well run companies of any age with great leaders and solid business models can produce very exciting results with a bit of patience.

P.S. Don’t forget to automatically re-invest the dividend.

Disclaimer: none of this is investment advice. Please do your own homework and invest carefully and thoughtfully.

Exhibit A: Microsoft transactions (includes some but not all dividend transactions)

This is a sample of Microsoft share transactions, including dividends re-investments. Not all years of dividends are included here.

Exhibit B: Meta transactions

These are Meta transactions, including dividends re-investments.

At the end of 2019, I bought a book on Audible for 1 credit (each credit costs me $14.95 in my Audible subscription plan). The book was called A Simple Path to Wealth by JL Collins. I listened to it on my annual Personal Offsite as I took time to reflect on the past year and to get energized for the year (and years) ahead.

The simple takeaway from this book reinforced what I was already doing: buying Vanguard index funds. However, JL narrowed it down even further. He famously suggested one specific index fund – VTSAX (Vanguard Total US Stock Market Index). His recommendation was a bit more nuanced than this and he suggested some other index funds as bubble wrap around this anchor tenant of a portfolio, but he made a solid argument for this financial product (it provides exposure beyond the US because US companies do a lot of business internationally; it is self cleansing, which means underperforming stocks naturally come out of the index and get replaced by new better performing stocks; etc.).

To make the long story short, three months after finishing the book, I started to follow the simple and crystal clear advice of dripping cash into VTSAX. As of this writing, after about five years of dollar cost averaging into this index fund, my paper gain is substantial and enough to buy me and my family a few years of memorable vacations (a double digit annual return in terms of %). Of course, that has a lot to do with the fact that the US stock market has performed well over that time (3/2020 to 7/2025), despite the pandemic. However, had I not listened to the book, I would not have done this. Of course, until I sell this fund, the gain is just on paper, but I will let it compound for a while longer. It is a very diversified fund, with ~3.5K US public companies in the index. By the way, the ETF version of this fund on Vanguard is VTI. VTI is basically the same thing as VTSAX and has some additional advantages like higher liquidity.

As with everything, this is not financial advice. VTSAX could easily go down 50% as the market has done a few times in the past. It is also not an endorsement of doing whatever one reads in a book. What I am hoping this illustrates is that books can hold extremely valuable ideas that can be super powerful when met with action. So, keep on reading and keep on investing.

A bonus action I took as a result of reading that book is starting this blog (JL started a blog before writing his first book: http://www.jlcollinsnh.com). Thanks, JL.

One of my favorite Seinfeld episodes is called “The Opposite.” In it, George (the perpetually unsuccessful main character) realizes that every decision he has ever made has been wrong, and that his life is the exact opposite of what he wanted it to be. His successful friend Jerry convinces him that if every instinct he has is wrong, then the opposite would have to be right. That feels pretty logical and George goes on to experiment with doing the complete opposite of what he would do normally. I won’t tell you what happens so as not to spoil it for you, but the basic concept from my favorite sitcom applies to investing.

The average investor tends to buy stocks when they are going up in price and tends to panic and sell when they fall. That is a very natural human behavior. However, it is not what leads to wealth creation. In fact, this basic behavior is probably what holds back most people who are actually on the right track (after all, not everyone even decides to save money to invest). There is a lot of literature on this but basically, the reason this holds people back is they tend to buy stocks when they are relatively high and sell when they are relatively low.

While the opposite strategy would be optimal, nobody can perfectly predict the highs and the lows. That’s why I tend to invest all the time (there has not been a month when I didn’t invest in at least 12 years but more likely in about 20 years). It’s not because I am so privileged that I can do this. I’ve invested various amounts, sometimes only a few hundred dollars in a 401k. It’s all about the discipline that helps me ultimately get the average price through time (not relatively low or high). I’ve written about dollar cost averaging in past posts (for example, here).

But this post is not about dollar cost averaging. I held back against my instinct to invest everything I had during the stock market party of 2021. Instead, I continued dollar cost averaging some money every month and holding some cash on the sidelines. I held off some cash so I can do the opposite of most people’s instincts. Most people sell during the “selloff,” when the market seems to be in free fall with the looming recession, Federal Reserve is steadily increasing the interest rate, and a major war is happening in Europe. I won’t perfectly find the bottom and I am not trying to. I’ve just increased the size of my monthly investments to make sure I get more of the “discounted” prices. I am still dollar cost averaging, but I am doing more to bring down the average.

For me, this is the time to put more of my cash to work. Like Warren Buffett, I expect to be a net buyer of stocks over the course of my life, which means I plan to buy more than sell. That means, I generally like it when stocks experience declines in price in the same way a shopper likes to shop during holiday promotions. As Mr. Buffett would also say, the world has gone through many selloffs and all kinds of calamities, but the stock market continues to grow when you zoom out far enough.

It’s a scary time for sure and I will most likely continue to see my portfolio go down in value. But 5-10 years from now and maybe even sooner, I will be glad I followed Jerry’s advice to “do the opposite.”

Here is a clip from that Seinfeld episode for further inspiration and a laugh.

I was reading Kiplinger and saw a reference to an app that helps parents to introduce kids to saving and investing. This app is called Greenlight and it allows you to send your child or children money to be used for various use cases: spending, saving, investing, and allowance.

It’s probably most useful for older children because one of the key features of the app is a debit card. However, I set it up for my 7-year old to get him exposed to some key personal finance concepts early.

I got him a debit card with his face on it for security and fun. The debit card he will use when he goes to the bookstore or toy store with me or other family members.

I was also very excited to get him to finally buy some stocks. We’ve been talking about buying shares of companies for a while and he’s been getting excited to become an owner. Finally, Greenlight was an easy way to get him going, without having to open some formal brokerage account.

Essentially, I took some money that he received for his birthday and sent it to his Greenlight account. Then, the fun began. He had $100 to work with and he really wanted to invest in companies that he believes are doing well. According to him, the companies he sees him or grownups using a lot are probably doing well and could grow in share price. For a basic analysis, that was good enough for me. That’s how he chose Disney and Apple, both very popular stocks in the app. I then guided him to also get some VOO (S&P 500 Vanguard ETF) to diversify his risk a bit and to have him be an owner of a lot of companies all at once. He really liked that idea.

At first he wanted to only invest $1 or $5 dollars into each stock, but I got him to really develop some conviction about his positions and he leaned in with $20 each. So, he invested $60 into the stock market and kept $40 in his Savings account.

As soon as he invested, the stock market took a hit, so he experienced that part of investing when you see your holdings go down in value. I was a bit bummed at first because I wanted him to really get excited about growth and investing. However, I felt it was good and real for him to also experience the downturn and to display some discipline to not sell. After a few days watching his stocks going down, he was definitely antsy to sell, but he held strong.

On the other hand, his Savings account gets 1% interest, so he also gained $0.02, which was small but nice to experience. Parents can increase this interest out of their pocket if they want the lesson of interest and compounding to be more clearly learned.

There are so many possibilities to explore and lessons to teach through this app, or a similar app. I get excited about thinking what results he might be able to see if he keeps investing small amounts into ETFs, such as VOO, and holds it for decades. Compounding makes young age so much more powerful than meets the eye.

The table below is from The Money Guy Show, one of my favorite podcasts on YouTube. In the table, you can see just how powerful age can be. For example, my son starting at age 7 has a ~394 money multiplier, which means his money will grow roughly that much from this age onwards without any additional contributions. That means that his invested ~$60 could turn into $23.6K by the time he is 65 years old. It also shows that if he puts away ~$26/month from now going forward, he will be a millionaire by the age of 65. It gets much harder to grow money when you start later; it’s obvious, but I hope this serves as a good visual reminder.

Note that there is a monthly subscription fee to get access to the app. I think it’s totally worth it to teach life-long lessons, but it will only make sense if he continues to be interested.

Disclaimer: If you click on my Greenlight link above and signup, we both get $30. All proceeds go to my son’s account and I recommend you do the same.

I admire Warren Buffett and very much look up to him. Unfortunately, I only started to follow him closely when I was in my 30s, after I met him in person. He has such a wonderful way of turning complex financial topics into simple digestible concepts that are very easy to understand and put into action.

When I look at his financial journey, I admire his annual return of about 20% vs. the S&P average (1965-2021). For me, the key reasons for his winning record are 1) picking the right companies to invest in, and 2) not trading their stock often because he thinks of them as businesses and not stocks.

But I think there is another reason why he is so wealthy. He has been investing for a very long time. At the time of this writing, Warren is 90 years old and he started investing when he was 11 years old. So he has been in the market for close to 80 years. Thanks to the power of compounding, one of Buffett’s favorite concepts, you don’t even have to be a financial genius to become wealthy if you have that kind of time horizon.

So, invest as early as possible (time in the market is more powerful and lucrative than timing the market), stay healthy to live longer, and make sure your kids get excited about investing and the freedom long-term investing will offer them.

The earlier you start, the better off you’ll be. This applies to many things in life, and certainly to personal finance. Here are some specific steps you can take:

Whether it’s your first paycheck or the first time you get money for your birthday, put some of it away into a brokerage account. A simple savings account is better than buying stuff, but you are much better off investing in stocks. The $100 you invest early in your life will do a lot more work for you than the same amount of money later in your life through this amazing thing called compounding (like a snowball, your money will grow faster and faster because it will keep adding to the base).

Set up an automated way for you to invest. I put money away towards investing every month automatically, and so should you. This will protect you from yourself and from human nature. The future you will really thank you for it. One of the coolest things about investing regularly is that it lets you dollar cost average (essentially, if a stock price for a given investment goes down, you are able to buy more of it with the same $100 and less of it if the price goes up).

Stocks is probably the asset class that will give you the highest return, so I recommend putting whatever you can allocate to investing to stocks. I think it’s fine to spend a little money on individual stocks of companies you know and in which you see potential. However, I recommend you invest in index funds (these funds simply track a number of companies). Key reasons why I like index funds are: a) they give you an easy way to diversify your risk across many companies, b) they are inexpensive because they are not actively managed.

Vanguard is my favorite brokerage company. John Bogle, who founded the company, is one of my heroes. He invented the concept of index funds and set up his company in such a way that really benefits investors with low costs and simplicity. Check out the index fund VTSAX (Vanguard Total Stock Market Index Fund). This fund basically covers the full United States stock market.

Consume content from which you can learn about personal finance (books, blogs, videos), especially from people who know what they are talking about: Warren Buffett, John Bogle, Napoleon Hill, JL Collins.

Invest your time wisely. You will spend most of your time in your job/career, so make sure that it’s something you love doing. Financially, if you pursue the business field like I did, strive to not just work for a paycheck. You can do this by either owning your own business or by working in companies, which give you stock as part of the compensation package. I have done the latter and have seen a significant return on my investment of time in the companies where I’ve worked.

Key takeaways and actions:

Always put away some portion of your income and do it regularly, ideally into a Vanguard index fund, such as VTSAX. Be a sponge and learn everything you can about personal finance. Be very strategic about your job and lean towards having ownership of the company stock.